Forward Contracts

Forward Contracts¶

Nature of the Forwards to be sold¶

The embedded volumetric optionality is primarily intended, at the time that the parties enter into the agreement, contract, or transaction, to address constraint factors that influence demand for transaction inclusion rights (i.e. blockspace). This instrument addresses the potential variability in the supply of available blockspace available for usage by different actors.

The options refer to slices of the overall gas size of β-blockspace. We aim to homogenize it, i.e. all slices of gas are equal and interchangeable. This is how the forward contract is exercised.

The nature of the forwards we are selling under the β-blockspace market depends on the capacity restriction we impose. Most importantly, do we guarantee enough capacity that the calls get included or not? The problem with guaranteeing a fixed capacity for β-blockspace is that this means restricting the capacity for ⍺-blockspace. The problem with this is that ⍺-blockspace might be more lucrative for us. In particular, we know that lottery blocks come along that make up a large chunk of the overall remuneration we can achieve at all.

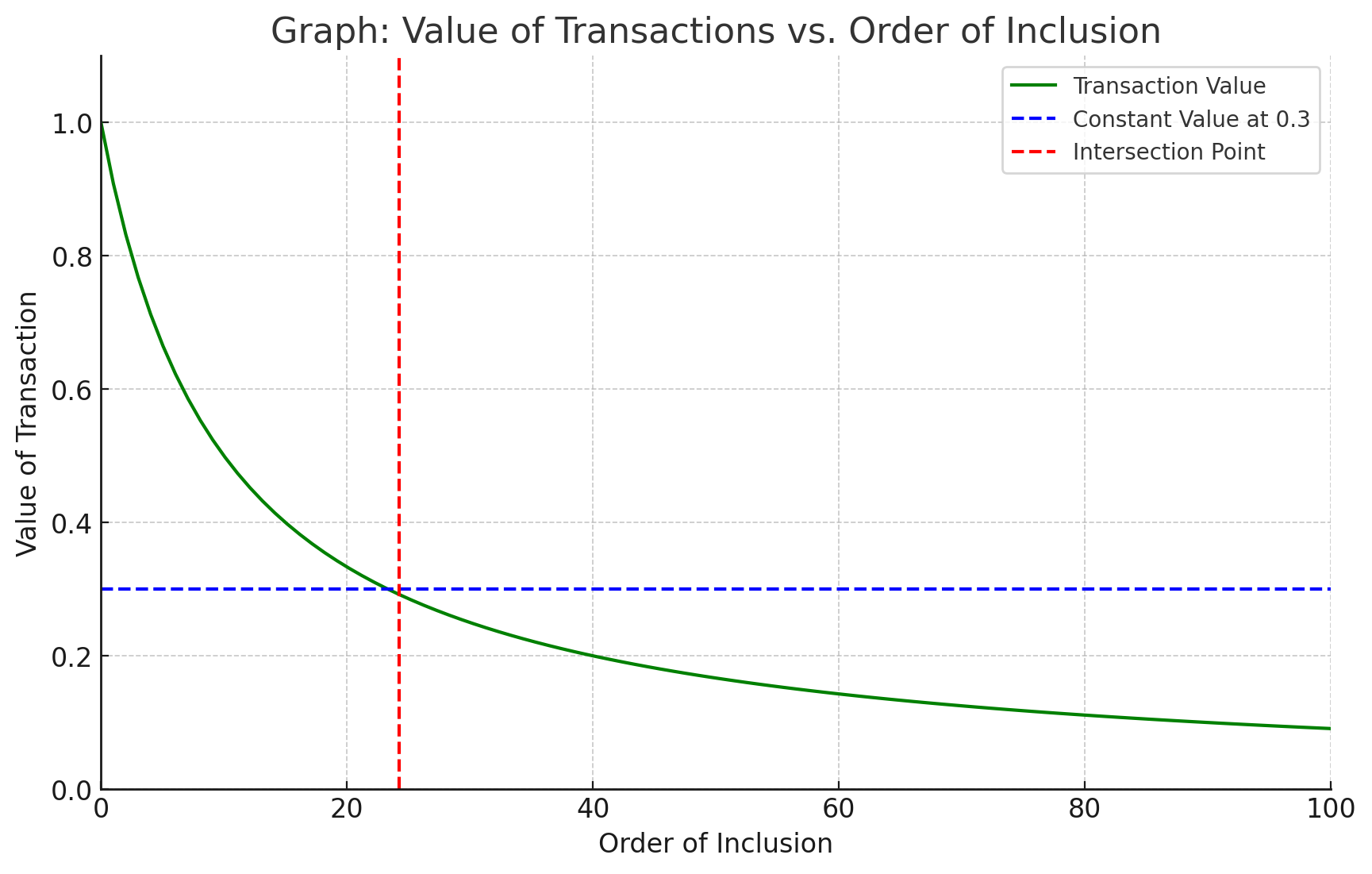

Figure 1: Tradeoff of ⍺/β-blockspace

If we fix ⍺-blockspace, we might be missing a significant amount of value. The tradeoff can be seen in the picture below.

We make the assumption that top of the block gas space is more valuable. The main assumption is that at some point, the marginal value for a builder owning the whole block (green) goes below the marginal value of a β-blockspace buyer (typically someone who wants to be just included independently of the order).

If we had perfect information, we could fix the capacity constraint at exactly the intersection point. But this information is not available. We can only approximate it. The question of lottery blocks can also be seen in the diagram, the question is whether for such a block both curves are shifted in the same way. If not, it would indicate the need to give ⍺-blockspace builders more space relative to β-blockspace builders.

Bidder characteristics¶

Assumption of Intrablock Position

We operate under the assumption that position does not matter; if it does might affect the design significantly.

-

Bidders are possibly risk-averse: Standard revenue equivalence might go out of the window. Bidders are asymmetric; in particular if there is private orderflow.

-

Bidders valuations are not clear: If they draw from a public mempool or if there are global conditions affecting value of block space, their valuations will be interdependent. - There is also the danger of a further coordination issue; this might favor a winner-takes-all solution

Relation to the secondary market¶

Traditionally we would assume that a well-designed auction does not require a secondary market. If the result of the auction is in the core, no change in the allocation makes sense. This is different here as information comes in overtime. - Base fee - Transactions updates for ⍺-blockspace bidders We operate under the assumption that position does not matter; if it does might affect the design significantly.

New bidders are active on the secondary market. The secondary market therefore is not just a reallocation of the primary auction but includes information updates.

Secondary Market Effects

This is in contrast to most work on auctions with resale (re: secondary) markets. The secondary market changes the rationale for bidding in the primary auction